19 de setiembre de 2025. Fitch Ratings reafirma la calificación crediticia BBB del gobierno de Uruguay como emisor de deuda en moneda local y de largo plazo, y mantiene la perspectiva estable. La calificación de Uruguay está respaldada por un PIB per cápita relativamente alto, indicadores de gobernanza e institucionales sólidos y finanzas externas robustas.

8 de mayo de 2025. Fitch Ratings publicó en su sitio web el resultado de la revisión sin comité de acción crediticia. No se publicó ningún comunicado de prensa. Acceda a los resultados haciendo clic aquí.

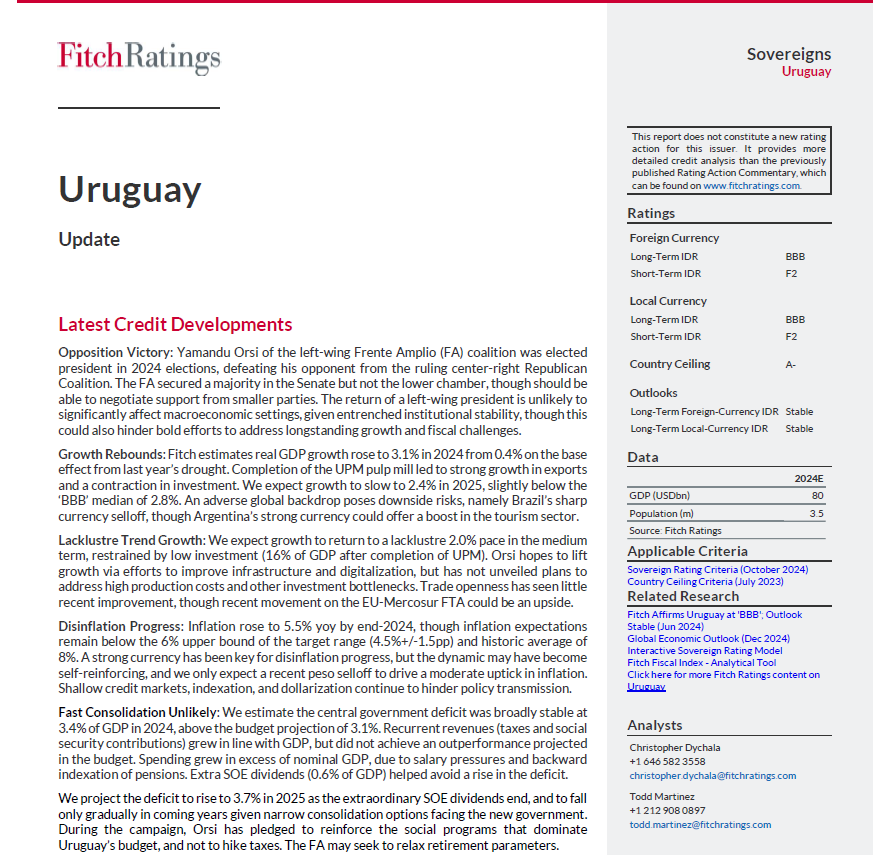

El 10 de enero de 2025, Fitch Ratings publicó una actualización de Uruguay con las ultimas novedades crediticias.

El 27 de noviembre Fitch Ratings publicó un comentario de mercado tras las elecciones presidenciales del 24 de noviembre.

Nueva York, 4 de junio de 2024. Fitch Ratings afirma las calificaciones de emisor en moneda local y de largo plazo de Uruguay en "BBB" con perspectiva estable. La calificación de Uruguay está respaldada por un PIB per cápita relativamente alto, indicadores de gobernanza sólidos y finanzas externas sólidas. La inflación de abril fue el nivel más bajo en casi diecinueve ańos y el undécimo mes consecutivo dentro del rango objetivo de BCU. La calificadora también mencionó que la regla fiscal ha mejorado la credibilidad y la transparencia.

El pasado 28 de marzo Fitch Ratings publicó un comentario de mercado evaluando la nueva institucionalidad fiscal y sus implicancias financieras en el Gobierno Central.

Fitch Ratings raised Uruguay´s Long-Term and Local Currency Issuer Ratings to BBB, and maintained a stable outlook. The rating upgrade reflects Uruguay´s resilient fiscal performance in absorbing the pandemic shock coupled with its record of compliance with its modified fiscal framework. The recent approval of a reform that improves the pension system's sustainability further signals the commitment to a more prudent fiscal policy consistent with its high governance scores.

Fitch Ratings confirmed Uruguay´s Long-Term Foreign and Local Currency Issuer Ratings at BBB-, and mantained the stable outlook. Uruguay's rating is supported by relatively high GDP per-capita, strong governance indicators and institutional strength evidenced by a successful pandemic response, and robust external finances.

4 de abril de 2022. Fitch Ratings publicó comentario sobre la no derogación de los 135 artículos de la Ley de Urgente Consideración, destacando que ello podrá catalizar las reformas económicas que el Gobierno tiene en agenda.

The revision of Uruguay´s Outlook to Stable from Negative reflects its fiscal resilience during the pandemic and further structural fiscal improvement. The rating is supported by high per capita GDP, strong governance scores and robust external liquidity. It is constrained by a record of weak economic growth and high inflation, high and heavily dollarised public debt, and policy flexibility weakened by dollarization, indexation and shallow financial depth.

Fitch Ratings confirmed Uruguay´s Long-Term Foreign and Local Currency Issuer Ratings at BBB-, and improved the outlook to stable from negative. The stable outlook reflects its fiscal resilience through the pandemic and ongoing improvement in the structural fiscal position. Fitch projects these developments will substantially slow the upward path of debt/GDP, with a narrower gap to rating peers than seen pre-pandemic.

Uruguay's Negative Outlook reflects high, rising public debt/GDP and uncertain prospects for fiscal consolidation and stronger economic growth needed to arrest this trend. Strong governance, per capita GDP and external liquidity support the rating, and balance low economic growth, high inflation, structural issues constraining policy flexibility, and high foreign-currency debt rendering public finances sensitive to exchange-rate movements.

To accommodate a higher frequency of rating reviews during the coronavirus pandemic, Fitch is publishing scaled-down Sovereign Rating Reports that focus on data and forecasts encompassed in reviews. For the rating rationale, refer to the Rating Action Commentary published on October 8th, 2020.

Fitch Ratings affirmed Uruguay's Long-Term Foreign-Currency Issuer Default Rating at BBB- with a Negative Outlook.The Negative Outlook reflects deterioration in growth and public finances that has been compounded by the coronavirus shock, and risks to government plans to arrest these trends.

Sluggish growth and structural fiscal deterioration are driving a rise in public debt at already high levels. The new centre-right government of Luis Lacalle Pou has expressed a clearer and more credible commitment to reverse these trends, but faces a weaker-than-expected starting point, difficult trade-offs, and implementation challenges.

Growth underperformance and fiscal deterioration have persisted, lifting the government debt burden and constraining policy space to confront shocks. The scope, nature and timing of potential measures to address these negative fiscal and macroeconomic trends remain uncertain, but could become clearer after the October 2019 elections.

Uruguay's ratings are supported by high social development and strong institutions, healthy external finances, and long-dated public debt and liquidity buffers mitigating fiscal financing risks. Persistent fiscal deficits and a high, rising debt burden are eroding policy space to confront shocks, against a more challenging economic backdrop.

Uruguay's ratings are supported by strong structural features in terms of social and institutional development, a healthy external balance sheet, and the sovereign's favourable debt maturity profile and financing buffers. These factors are balanced by a weak track record of compliance with inflation and fiscal targets.

Ratings are supported by strong structural features in terms of social and institutional development, a strong external balance sheet, and fiscal financing buffers. These factors are balanced by a weak record of compliance with inflation and fiscal targets, weighing on policy credibility, a high and dollarised public debt burden, and budget rigidity.

Uruguay's ratings are supported by strong structural features in terms of social and institutional development, solid external buffers, and low fiscal financing risks. These factors are balanced by high inflation, high public debt, and a rigid spending profile lifting fiscal deficits above targets in recent years.

Uruguay's creditworthiness is supported by strong structural features in terms of social and institutional development, established external buffers and low fiscal financing risks.

Uruguay's creditworthiness is supported by its strong institutional quality, social stability underpinned by high income and human development, and buffers that have enabled solid growth performance despite external challenges.

Uruguay's ratings are underpinned by strong structural factors including high per capita GDP and social development indicators, as well as strong institutional quality. Strengthened external buffers, an improved debt profile and higher growth in relation to peers have also supported creditworthiness.

Fitch Ratings upgraded Uruguay's Foreign- and Local-Currency IDRs to BBB- and BBB, respectively, in March 2013. Economic resilience in difficult external conditions, together with a stronger external balance sheet and improved debt profile support the upgrade.

Fitch Ratings affirmed Uruguay's Foreign and Local-Currency IDRs at BB+ and BBB- respectively with a Positive Outlook on 23 April 2012. This reflects reduced external and fiscal vulnerabilities underpinned by stronger international liquidity and improved currency composition of government debt.

In this report Fitch Ratings looks at Uruguay's current progress in creditworthiness compared with other BB+ sovereigns that successfully made the transition to the investment grade (IG) category.

On 14 July 2011 Fitch Ratings upgraded Uruguay's Foreign-Currency IDR to BB+ from BB and Local-Currency IDR to BBB- from BB+. The Outlook is Stable.